When you're trading crypto, price isn’t the only number that matters. Whether you're a beginner placing your first market order or a seasoned trader moving serious volume, two subtle but crucial concepts can quietly impact your returns: the bid-ask spread and slippage.

These trading mechanics often go unnoticed—until they start eating into your profits. Here’s what they are, how they work, and how to manage them.

What Is the Bid-Ask Spread?

Every time you look at a trading pair on an exchange, you're seeing two key prices: the bid (what buyers are offering) and the ask (what sellers are asking). The bid-ask spread is the gap between them.

If you're buying instantly, you’ll pay the lowest ask. Selling? You’ll receive the highest bid. That difference—the spread—is the cost of immediate execution.

In highly liquid markets like Bitcoin or forex, this spread is razor-thin. In lower-volume assets or volatile tokens, it widens. A tight spread often means a healthy, competitive market. A wide one? It signals low liquidity and a higher cost to trade.

Example:

If BNB has a bid of $800 and an ask of $801, the spread is $1. In percentage terms:

801−800801×100=0.125%\frac{801 - 800}{801} \times 100 = 0.125\%801801−800×100=0.125%

Now compare that to a thinly traded meme coin with the same $1 spread on a $10 price. That’s a 10% spread—an expensive trade just to get in or out.

Who Creates the Spread?

In traditional markets, brokers and institutional market makers create liquidity and pocket the spread as profit. In crypto, especially on centralized exchanges, liquidity mostly comes from other traders placing limit orders. Still, some exchanges rely on professional market makers, who profit by rapidly buying low and selling high across that spread.

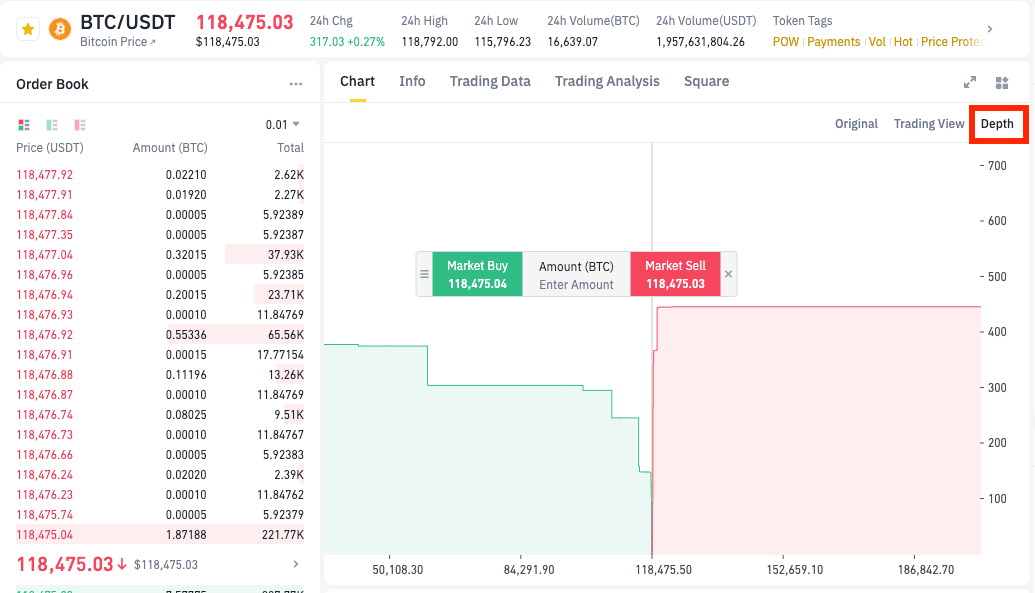

This role becomes obvious on a depth chart, like the one you’ll find on Binance. The chart visualizes all active buy and sell orders, showing how many traders are waiting at each price level. The narrower the visible gap between green (bids) and red (asks), the healthier the liquidity.

Slippage: When Price Moves Against You

Slippage happens when your order doesn’t fill at the price you expected. This is common when trading volatile tokens or placing large market orders that consume multiple levels of the order book.

Real-world example:

You place a market buy at $100, but there aren't enough sellers at that price. The exchange matches your order with higher-priced sellers until it’s filled—raising your average buy price to, say, $104. That $4 difference? That’s slippage.

This problem is especially pronounced on decentralized exchanges (DEXs) and with tokens in low-liquidity pools. Sometimes slippage can exceed 10%, which is brutal on large trades.

Can Slippage Be Positive?

Yes—though it’s rare. If the price moves in your favor before your order executes, you might end up buying for less or selling for more than expected. This is called positive slippage.

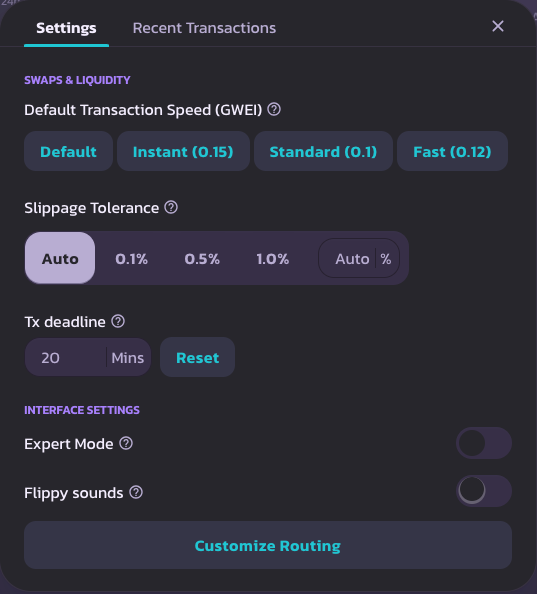

Slippage Tolerance and Front-Running

On DEXs like Uniswap or PancakeSwap, you can set a slippage tolerance, which caps how far you’re willing to deviate from your target price. But be careful: setting it too high can expose you to front-running, where bots or faster traders jump ahead of your transaction and profit off the difference.

How to Minimize Slippage

- Break large trades into smaller chunks.

- Stick to liquid markets where trading volume is high.

- Use limit orders instead of market orders to control execution price.

- Monitor network fees—on-chain transaction costs can quickly add up.

Final Thoughts

Bid-ask spreads and slippage won’t make headlines, but they quietly shape every trade you make. For casual traders, they may seem negligible—but at scale, they can erode returns fast.

Understanding how they work gives you better control over your trades, especially in volatile or low-liquidity environments like DeFi. Whether you're trading Bitcoin or chasing the next meme coin, knowing your costs before you click “Buy” can make all the difference.