Strategy shares traded near $130 Thursday after Benchmark reiterated its “buy” rating and backed the firm’s pivot to its perpetual preferred, STRC. The call signals analyst support for a funding model designed to accelerate bitcoin per-share growth despite recent market pressure.

Executive Chairman Michael Saylor outlined the shift during his keynote at Strategy World 2026 in Las Vegas on Wednesday. He said the company will move away from urging corporate balance sheet adoption and instead position STRC as the primary vehicle for financing future bitcoin purchases.

📹 WATCH: @Saylor delivers his keynote speech on Digital Credit at Strategy World 2026.

— Bitcoin For Corporations (@BitcoinForCorps) February 25, 2026

He unpacks #Bitcoin as Digital Capital, explains how variable preferred equity (STRC) unlocks long-duration, tax-efficient yield with principal protection, and outlines a future where ETFs,… pic.twitter.com/Pvih8MuZo1

Can STRC Sustain Bitcoin Accretion?

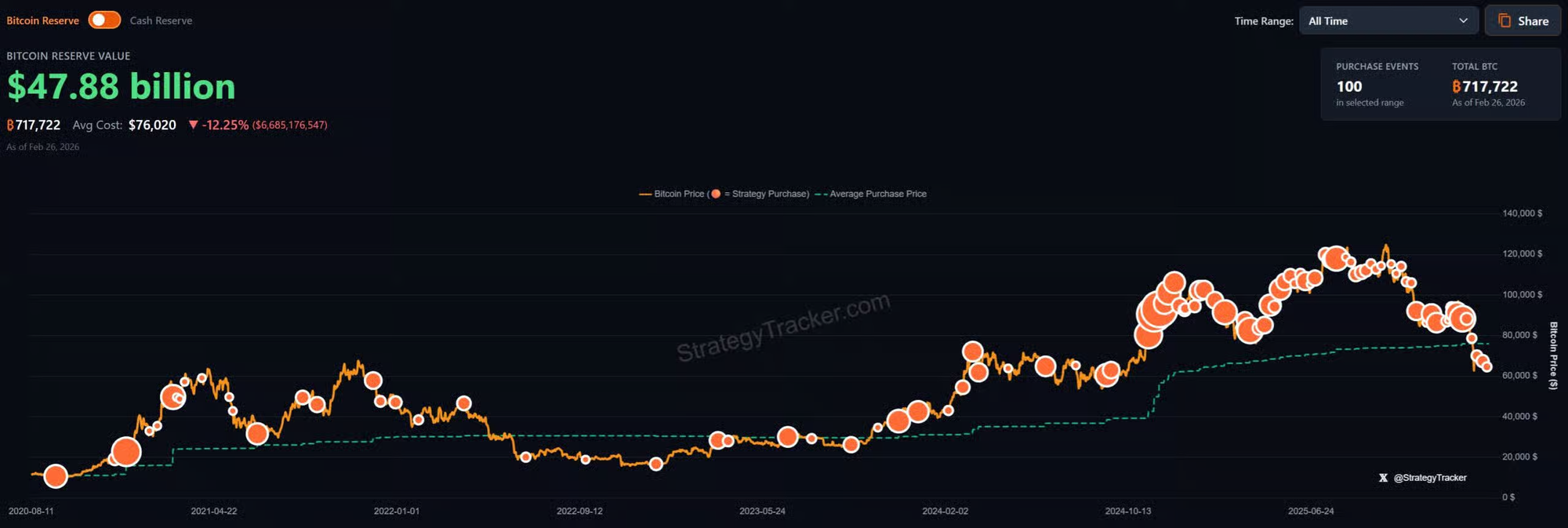

Strategy holds 717,722 BTC, representing more than 3% of total supply, and continues adding through equity and preferred issuances. Yet the firm is sitting on more than $6.7 billion in unrealized losses on its bitcoin position, according to Saylor Tracker data, as prices remain below late-2025 highs.

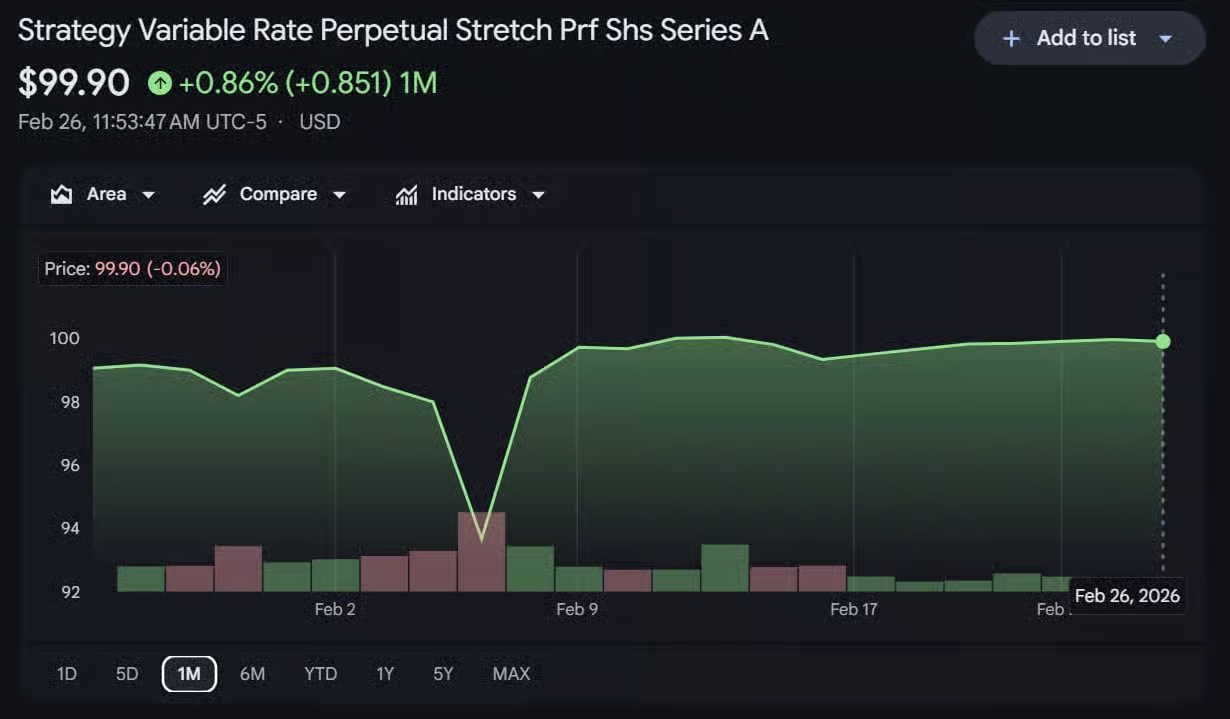

STRC, which dipped to $90 earlier this month, has rebounded to just under its $100 par value and offers an effective annual yield of roughly 11% with monthly dividends and seniority over common shares. Benchmark analyst Mark Palmer described STRC as the “primary engine” for funding bitcoin accumulation, adding that protecting its price stability now guides capital allocation decisions.

Palmer maintained a $705 price target based on projected year-end 2026 bitcoin holdings, a multiple on expected BTC gains, and the value of Strategy’s legacy software business. But the structure depends on Strategy’s common stock continuing to trade at a premium to net asset value, enabling accretive capital raises that expand holdings per share.

Saylor framed the pivot as part of a broader “digital credit” model, casting bitcoin as “digital capital” convertible into yield-bearing instruments rather than directly held treasury assets. The next catalyst will be whether sustained STRC demand allows Strategy to resume materially expanding its bitcoin position while stabilizing preferred pricing.