Stablecoins, once viewed mainly as tools for crypto traders, are rapidly evolving into something more practical: everyday money.

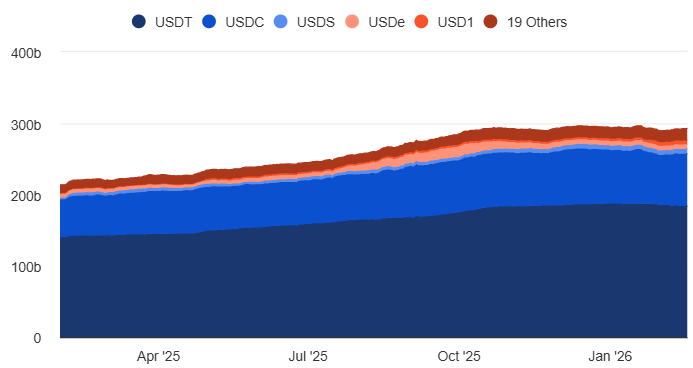

A new global survey published in The Stablecoin Utility Report 2026 suggests that the more than $300 billion circulating in dollar-pegged stablecoins is increasingly being used for payments, payroll, savings, and cross-border work — not just trading. The research was conducted by BVNK in partnership with Coinbase and Artemis, based on responses from 4,658 adults across 15 countries.

From Trading Tool to Financial Utility

Stablecoins are cryptocurrencies designed to hold a steady value, typically pegged 1:1 to fiat currencies like the U.S. dollar. The market is dominated by Tether and Circle, whose dollar-backed tokens make up the bulk of the roughly $300 billion supply.

The report suggests that these digital dollars are moving beyond exchanges and into personal finance.

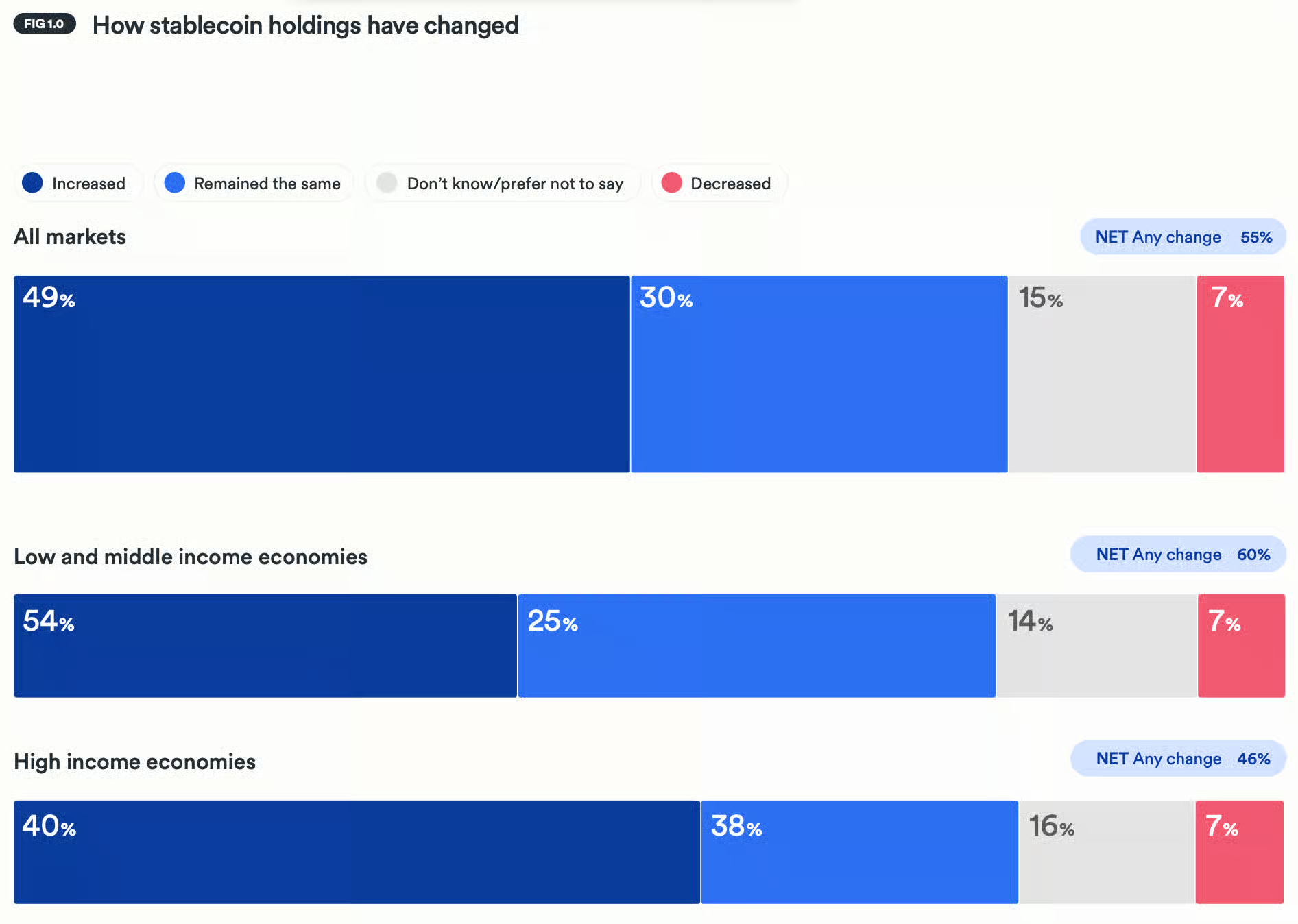

More than half of survey respondents said they had held stablecoins in the past year. Among current holders, 56% plan to acquire more within the next 12 months, while 13% of non-owners say they intend to start. Half of existing holders increased their balances over the past year.

On average, respondents said they allocate about one-third of their total savings to crypto assets and stablecoins combined. Adoption is particularly strong in low- and middle-income economies, where currency volatility and limited access to reliable cross-border payment systems make dollar-linked digital assets appealing.

Africa recorded the highest ownership rates in the survey, along with the strongest forward intent to buy more stablecoins.

This trend aligns with separate estimates from Standard Chartered, which has suggested that as much as $1 trillion could eventually shift from emerging market bank deposits into U.S. dollar-backed stablecoins.

Spending, Remittances, and Cross-Border Work

The data indicates that stablecoins are not simply being held as digital savings.

Among holders:

- 27% said they use stablecoins directly to pay for goods and services.

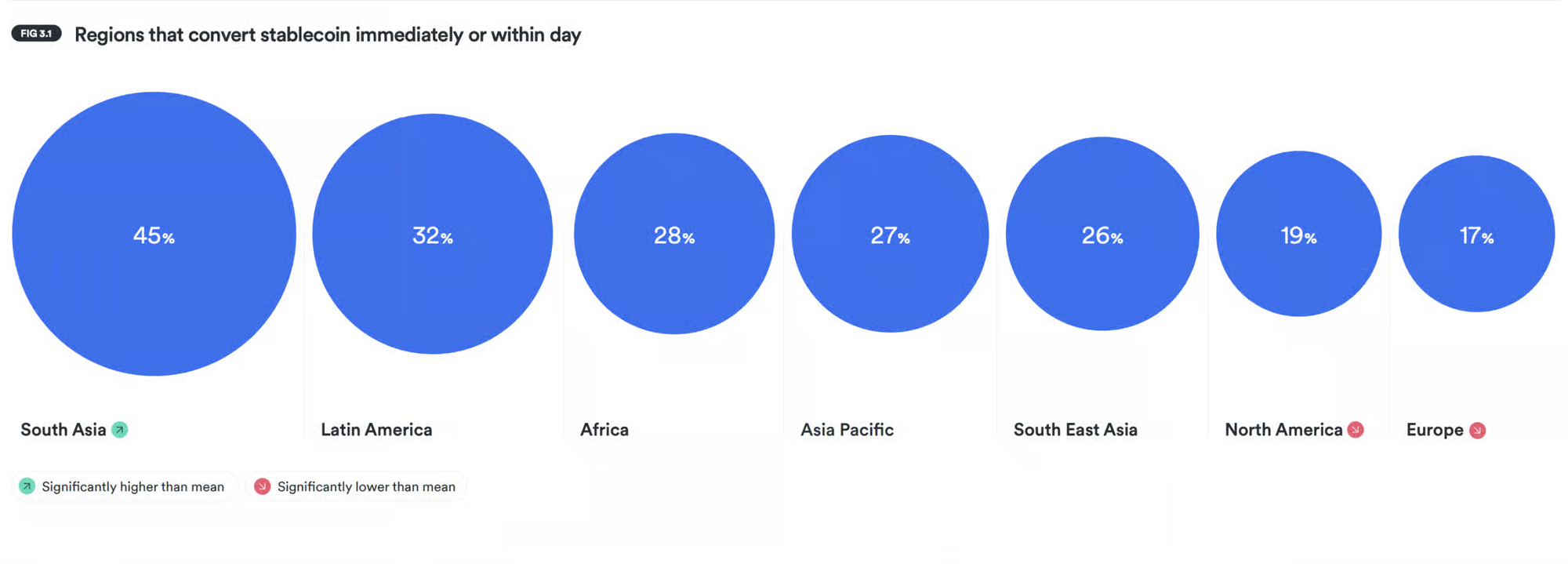

- 45% convert them into local currency for spending.

- More than one-quarter spend or convert their tokens within days.

- Around two-thirds do so within a few months.

Merchant demand appears to be rising. Over half of respondents said they had made a purchase specifically because a business accepted stablecoins. Across everyday purchases and larger expenses alike, reported interest in spending stablecoins exceeds current levels of usage.

For cross-border workers, the role of stablecoins is even more pronounced. Freelancers, gig workers, and marketplace sellers who receive stablecoin payments said the tokens account for roughly 35% of their annual income on average. Nearly three-quarters reported that stablecoins improved their ability to work with international clients, and a similar share of marketplace sellers said their sales volumes increased or their customer base expanded.

Cost savings are a major driver. Respondents receiving payments or remittances in crypto reported saving about 40% in fees compared with traditional financial services. Lower transaction costs, enhanced security, and the ability to transact globally were cited as top reasons for choosing stablecoins.

Friction Points Remain

Despite the growth, barriers remain.

Users highlighted concerns about irreversible transactions, the risk of losing funds, complex wallet management, and confusion around blockchain selection. Many respondents said they want stablecoin payments to resemble mainstream financial systems, with clear fees, broader merchant acceptance, and stronger consumer protections.

In other words, while adoption is expanding, usability still needs refinement.

Regulatory Momentum Builds

The study comes at a time of increasing regulatory focus, particularly in the United States.

Under President Donald Trump, lawmakers recently passed the GENIUS Act and are negotiating a broader federal framework that includes oversight for dollar-backed stablecoins. Industry participants say debates continue around whether stablecoin issuers should be allowed to offer yield, and there is urgency to finalize rules before upcoming midterm elections.

Greater clarity could influence how quickly stablecoins transition from niche financial tools to widely accepted digital cash alternatives.

A Turning Point for Digital Dollars?

The findings suggest stablecoins are steadily embedding themselves into daily financial life, particularly in regions where traditional banking infrastructure is costly or unreliable.

If regulatory frameworks mature and user experience improves, stablecoins may continue shifting from speculative assets to practical instruments for saving, spending, and earning across borders.

For millions of users worldwide, they already function less like crypto — and more like money.