The aftermath of a late-December exploit on the Flow blockchain continues to ripple through its ecosystem, with NFT-backed loans emerging as one of the most affected areas. While the Flow Foundation says user balances were not compromised, a temporary network shutdown has left some borrowers unable to repay loans on time, creating uncertainty for both lenders and NFT holders.

The incident occurred on December 27, when Flow paused its Cadence execution environment as a precautionary measure. The pause lasted until the morning of December 29. During that window, users were effectively locked out of normal blockchain activity, unable to move tokens or interact with smart contracts. For borrowers with loans maturing during those two days, the timing could not have been worse.

🚨 VERY IMPORTANT – PLEASE READ 🚨

— Flowty (@flowty_io) December 30, 2025

As you have likely seen, @flow_blockchain was exploited on December 27. According to the Flow team, no user assets or balances were impacted as part of the exploit. In response, the Flow team initiated a blockchain pause that lasted until 10…

Flowty, a lending platform that allows users to borrow against NFTs on Flow, reported that 11 loans reached maturity while the network was frozen. Only one of those loans was successfully repaid through an automated payment system. Eight loans defaulted, and two others failed to settle due to account restrictions linked to the exploit response.

Although Flow has since brought its network back online, many core services remain impaired. Token swaps are still largely unavailable, making it difficult for borrowers to obtain the assets needed to repay outstanding loans. As a result, some users who may be willing and able to repay remain blocked by technical limitations beyond their control.

To prevent further disruption, Flowty took the unusual step of pausing loan settlements altogether. As of 2:15 p.m. ET on December 30, the platform stopped processing repayments and defaults. Any loans maturing during this period will neither settle nor default. Instead, they remain open in what Flowty has described as a state of “limbo.”

The decision effectively freezes activity on both sides of the lending market. Lenders will not earn additional interest on paused loans, while borrowers cannot repay and reclaim their NFTs, even if they already hold sufficient funds. Flowty said the move was intended to avoid forced defaults caused by network-wide issues rather than borrower behavior, particularly where valuable or irreplaceable NFTs are at stake.

The platform also disabled new loan listings and removed existing ones from its marketplace to limit further exposure until conditions stabilize. Flowty has indicated it plans to introduce a defined repayment window once broader ecosystem functionality is restored, though it has not provided a specific timeline.

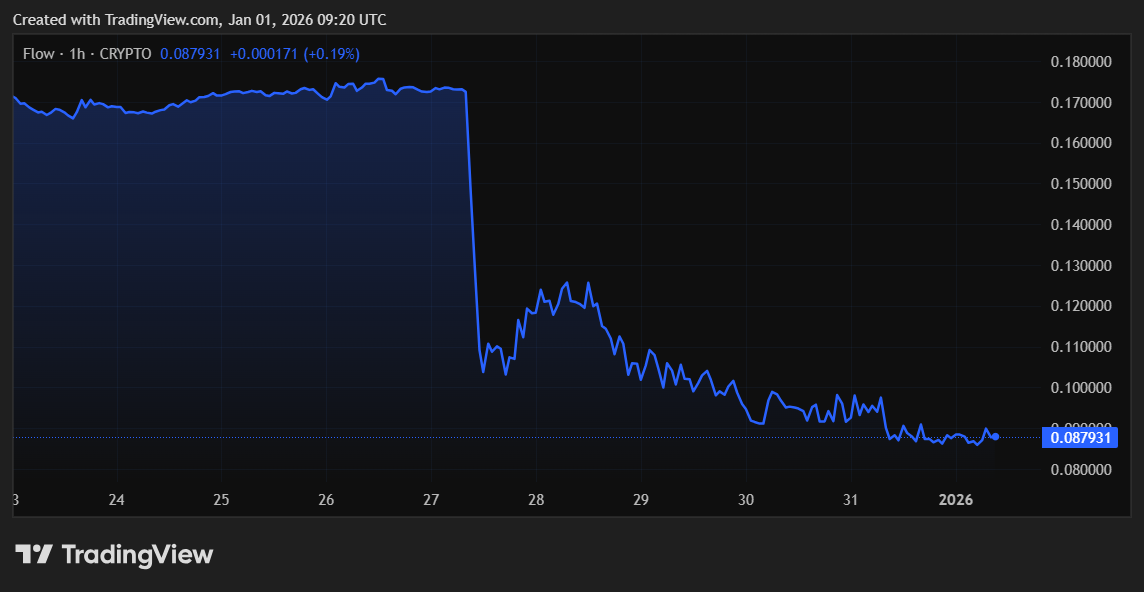

Meanwhile, market confidence in Flow has taken a hit. The network’s native FLOW token fell about 40 percent in the immediate aftermath of the exploit and has declined a further 17 percent since then. As of press time, FLOW was trading around $0.086, according to data.

The Flow Foundation has maintained that the exploit did not result in lost user funds, but the episode has highlighted how infrastructure-level disruptions can cascade into higher-level applications such as lending. For borrowers and lenders alike, the current situation underscores the risks that come with relying on complex, interconnected blockchain systems.

As Flow works to restore full functionality, users across the ecosystem are watching closely. The coming weeks will likely determine how quickly confidence can return and whether temporary measures like paused settlements are enough to protect participants from long-term damage.