Bitcoin on the Balance Sheet: A Boon or a Risk for the Market?

As corporate adoption of Bitcoin accelerates, a growing number of companies are converting their treasuries into crypto vaults. What began with MicroStrategy’s bold pivot has become a broader trend—publicly traded firms holding over 4% of all Bitcoin in circulation. But while the strategy may offer benefits like diversification and inflation hedging, some analysts are asking: what happens if the market turns?

Could these Bitcoin-heavy balance sheets become a liability, not just for companies, but for the entire crypto market?

The Rise of Bitcoin Treasury Strategies

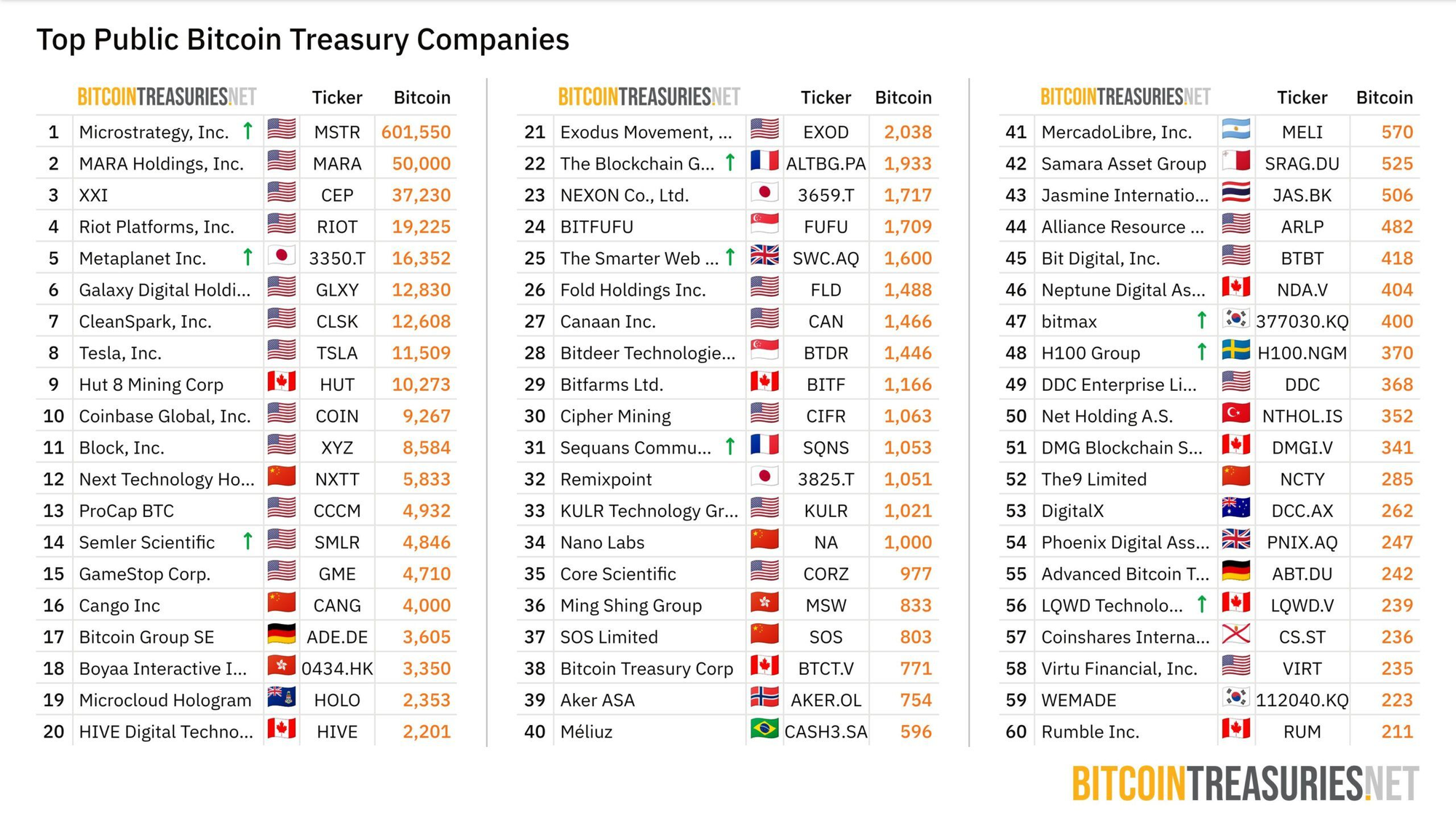

More than 60 companies have joined the ranks of Bitcoin treasury holders in 2025 alone, according to public filings. Some, like MicroStrategy (now rebranded as Strategy), have gone all-in—making Bitcoin the centerpiece of their business model. Strategy holds over 580,000 BTC and has built a playbook that others are now trying to replicate.

Others, including GameStop and PublicSquare, have taken a more cautious approach. They hold Bitcoin as a hedge but remain focused on their core operations. This diversification provides a buffer during market downturns—a layer of protection pure-play Bitcoin firms often lack.

Valuing Bitcoin Treasury Companies: More Than Just the Holdings

When a company shifts to a Bitcoin-first model, its value becomes tethered to its BTC holdings. But to outperform Bitcoin itself, firms must convince investors that their shares are worth more than the underlying crypto.

Strategy does this by continually increasing the amount of Bitcoin per share. Through capital raises, convertible debt, and At-The-Market (ATM) stock offerings, it turns investor confidence into more Bitcoin—amplifying the value of each share.

This creates what’s known as the Multiple on Net Asset Value (MNAV): a premium over the actual Bitcoin held. But maintaining that premium requires flawless execution, investor trust, and a rising Bitcoin price.

The Fragile Economics of a Bitcoin Premium

The MNAV model only works as long as companies can raise funds at favorable terms and the market believes in their growth story. Strategy can issue debt at low interest rates due to its size, reputation, and the cult-like following of its leadership.

Smaller companies face steeper challenges. Lacking creditworthiness, they often secure expensive financing or must overleverage. If Bitcoin’s price drops, margin calls or debt defaults can cascade across multiple firms—especially those that have few or no alternative revenue streams.

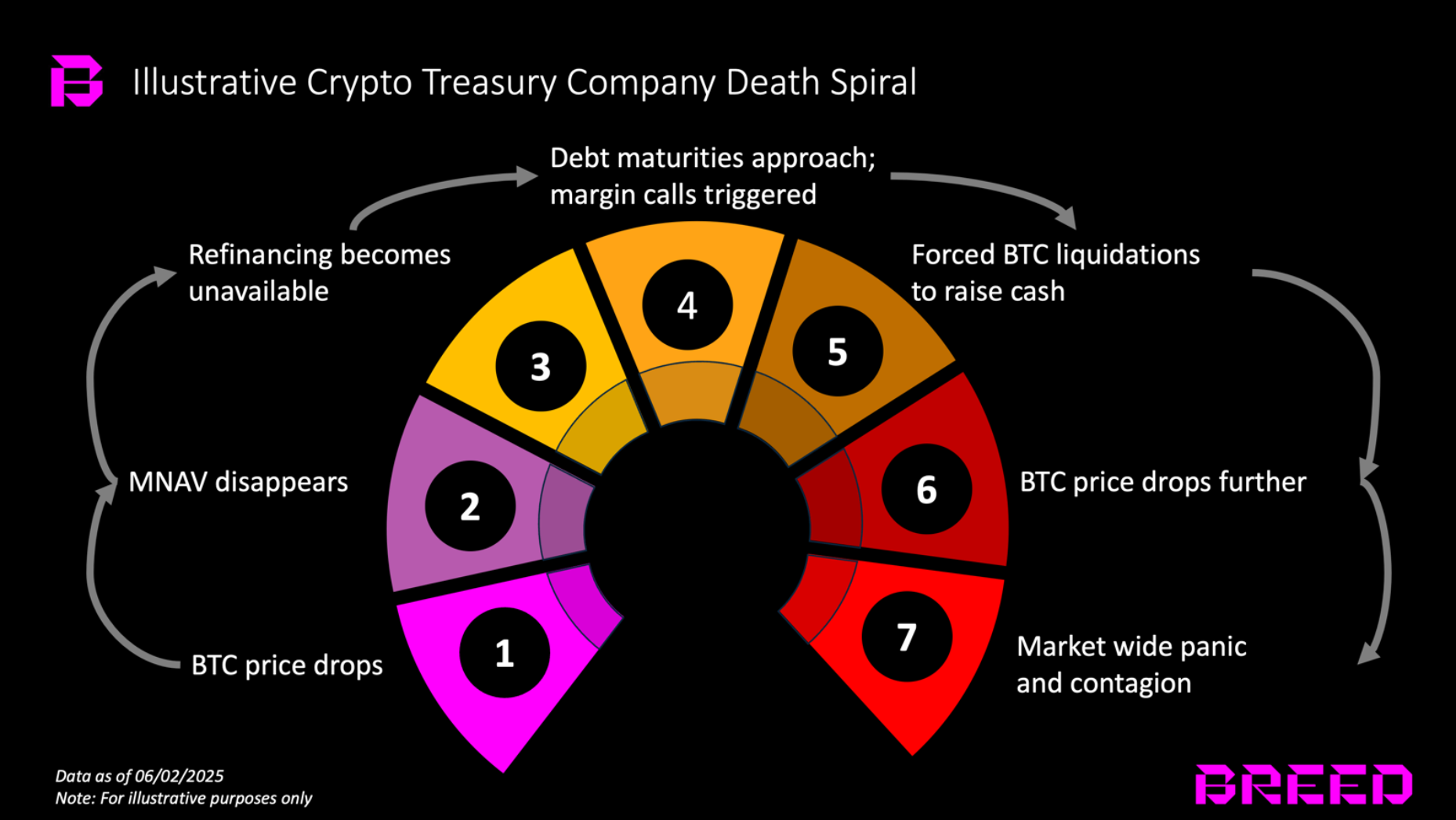

The Risk of a Reflexive Sell-Off

If a downturn hits and Bitcoin-first companies are forced to sell, it could trigger a chain reaction. Distressed sales by one firm would depress prices, pushing others into similar financial stress. The result: a self-reinforcing loop of selling pressure, known as a reflexive death spiral.

This is no theoretical risk. The 2022 bear market exposed how quickly leverage, speculation, and limited liquidity can turn optimism into a rout. If dozens of companies holding large Bitcoin reserves go under simultaneously, the fallout could rival—or surpass—previous crypto crises.

Should Companies Go All-In on Bitcoin?

Strategy’s success as an early mover doesn’t guarantee a blueprint for others. Most firms don’t have a Michael Saylor or access to billions in convertible debt. They also lack the brand power to command a consistent MNAV premium.

For these reasons, companies must tread carefully. Adding Bitcoin to a balance sheet can be a smart hedge—but transforming into a full-fledged Bitcoin treasury holding company carries systemic risks. The crypto market's bullish streak could reverse quickly if too many players bet the farm.