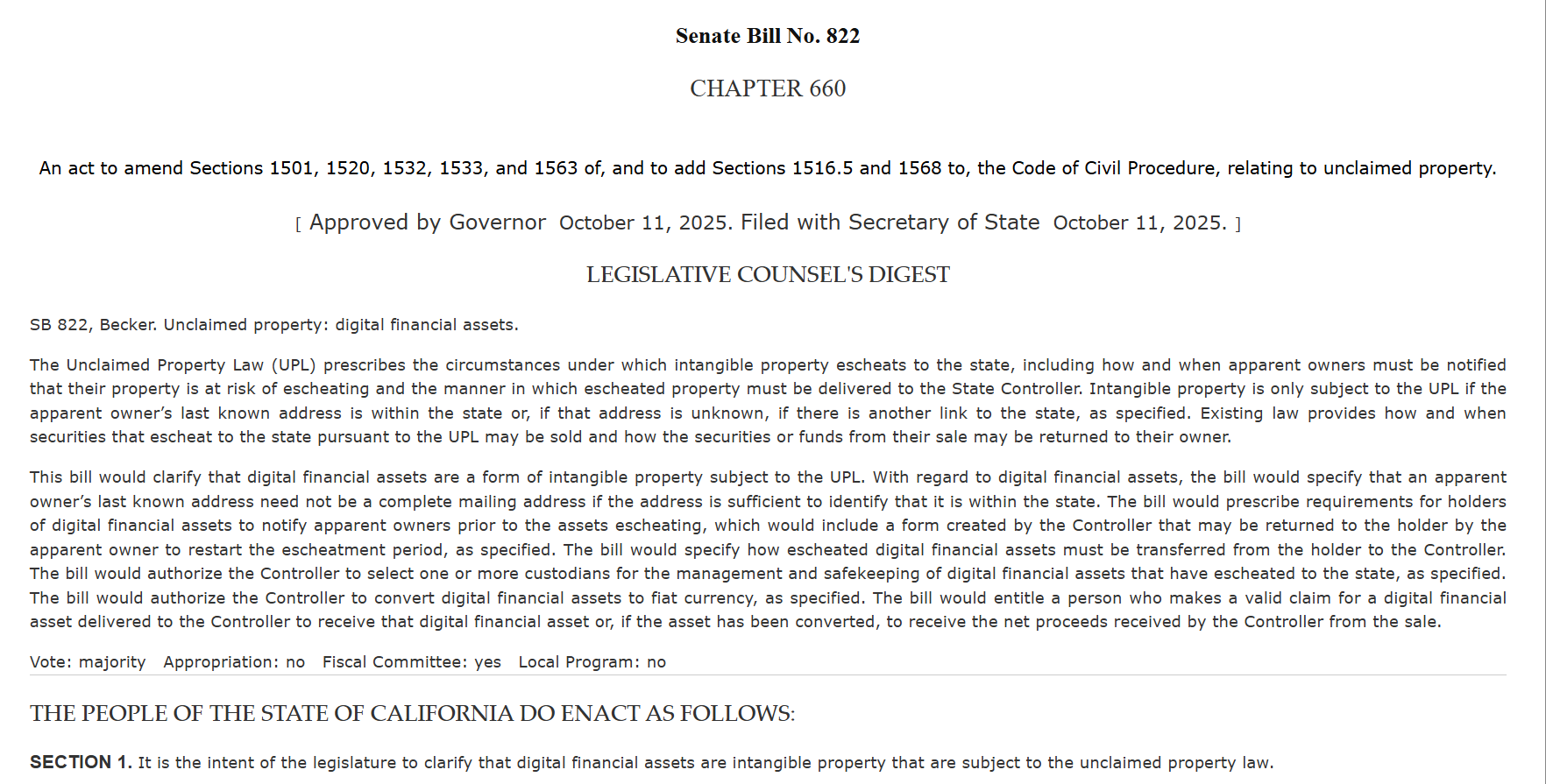

California has officially updated its property laws to include digital assets, becoming one of the first U.S. states to ensure unclaimed cryptocurrencies are preserved in their original form rather than converted into cash.

Governor Gavin Newsom signed Assembly Bill 1052 (AB 1052) and Senate Bill 822 (SB 822) into law this week, modernizing the state’s Unclaimed Property Law to account for cryptocurrencies like Bitcoin and Ethereum. The legislation requires that crypto assets left inactive for three years on custodial platforms—such as exchanges—be transferred to the state for safekeeping, without being liquidated.

This means that if a California resident forgets about or abandons a crypto wallet held on an exchange, those assets will be securely stored by the state in their original digital form. The assets will remain available for the rightful owner to reclaim at any time, rather than being sold and converted to fiat currency upon transfer.

“This is a win for consumer protection and digital asset rights,” said Paul Grewal, chief legal officer at Coinbase, in a post on X. “Thank you [Governor Newsom] for signing SB 822, which stops the state from liquidating Californians’ unclaimed crypto investments without their consent.”

Thank you @GavinNewsom for signing SB 822, which stops the state from liquidating Californians’ unclaimed crypto investments without their consent. Also thank you @SenJoshBecker, who sponsored the bill. Now it's time for California to join the 46 other states, along with @secgov,…

— paulgrewal.eth (@iampaulgrewal) October 14, 2025

Sponsored by Senator Josh Becker, SB 822 establishes a framework for managing dormant crypto accounts—those left untouched for three or more years. The law classifies these holdings as intangible property, eliminating legal uncertainty around how digital financial assets fit into California’s traditional property reclamation system.

To safeguard the assets, the State Controller will appoint licensed custodians to securely manage unclaimed cryptocurrencies in compliance with state standards. These custodians will hold the assets in digital form until an owner steps forward. However, the bill allows for a conversion to fiat currency if no claim is made within 18 to 20 months after an account is officially reported as unclaimed.

The move signals California’s growing effort to align financial regulations with emerging digital technologies. By protecting unclaimed cryptocurrencies from forced liquidation, the state acknowledges the unique nature of digital assets—both as investments and as part of the broader evolution of finance.

As the world’s fifth-largest economy and home to Silicon Valley, California’s decision may serve as a model for other jurisdictions looking to balance consumer protection with crypto innovation.