Bitcoin is hovering just under the $70,000 mark, caught in a tug-of-war between improving inflation data and lingering structural weakness in the crypto market.

The world’s largest cryptocurrency by market capitalization was trading around $68,600 on Monday, according to data. The price briefly slipped below $70,000 late last week and has remained locked in a wide $60,000 to $72,000 range that has capped rallies for weeks.

Despite signs of cooling inflation in the United States, analysts say the broader setup leaves Bitcoin vulnerable to sharp moves in either direction.

Institutional Flows Remain Under Pressure

Recent fund flow data paints a cautious picture.

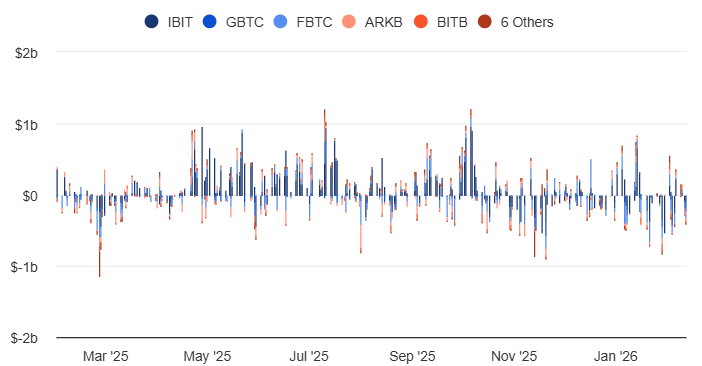

Timothy Misir, head of research at BRN, noted that crypto markets have stayed under pressure through mid-February as spot Bitcoin ETFs continue to record net outflows. Last week alone, spot Bitcoin ETFs saw roughly $360 million exit, while ether products experienced $161 million in net outflows. In contrast, smaller inflows were recorded for Solana and XRP spot ETFs.

Over the past four weeks, crypto exchange-traded products have shed approximately $3.7 billion, according to data from CoinShares, extending a broader pullback in institutional demand.

Even large investors appear to be repositioning selectively. Harvard University trimmed its Bitcoin ETF holdings by 21% while building an $87 million position in ether, signaling rotation within crypto rather than renewed risk appetite across the board.

On-Chain Metrics Suggest Quiet Accumulation

While fund flows remain negative, blockchain data offers a more nuanced view.

Bitcoin’s market value to realized value ratio is hovering near 1.1, approaching levels that historically suggest undervaluation. Meanwhile, net unrealized profit and loss metrics have slipped into what analysts describe as a “hope/fear” zone, often associated with late-stage corrections.

The spot price also sits below the short-term holder cost basis, estimated around $94,000, and beneath the so-called True Market Mean near $80,100. That dynamic suggests sustained pressure on more recent buyers.

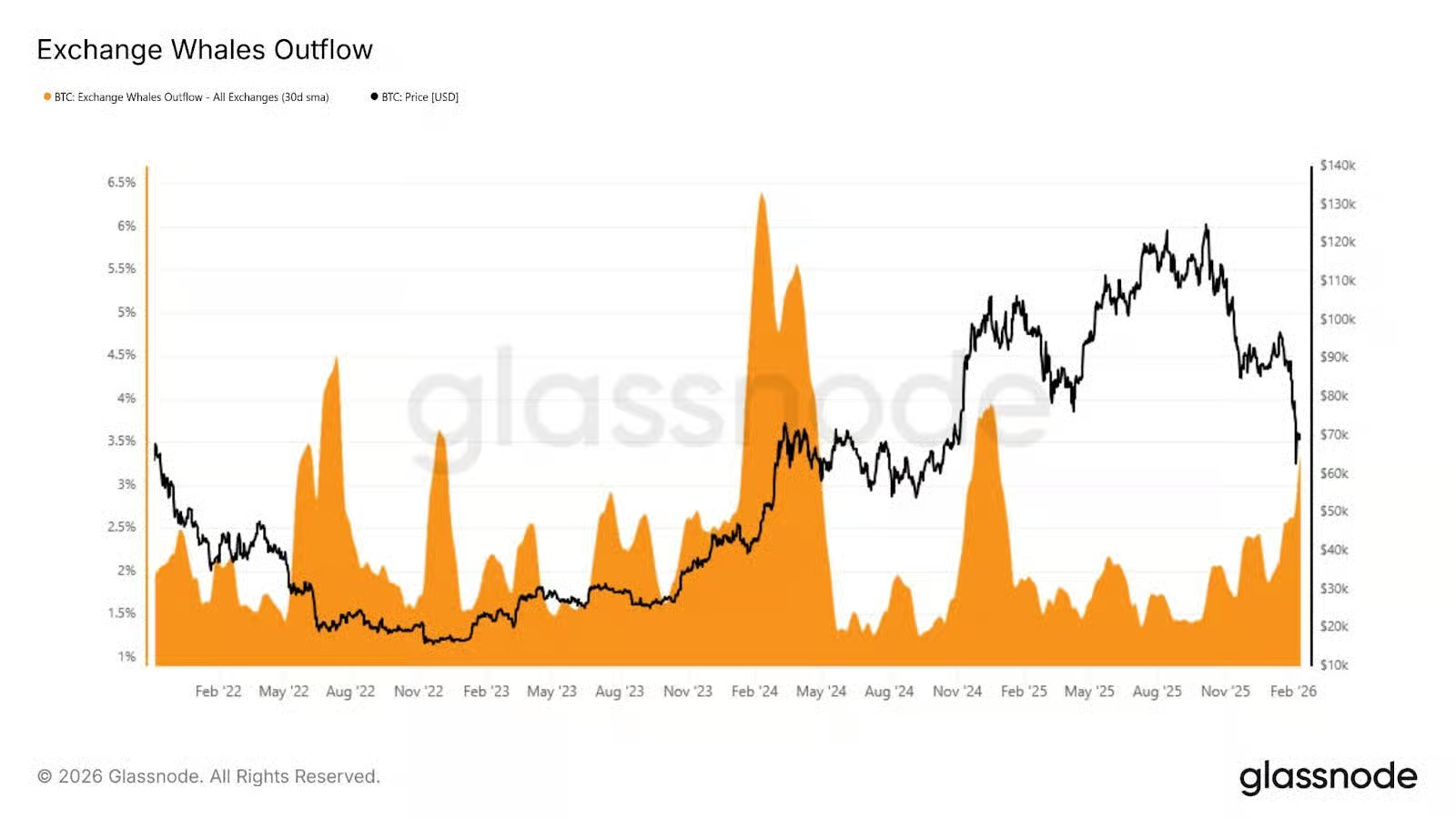

At the same time, exchange outflows to large entities have increased. The 30-day moving average of such outflows has risen to 3.2% since Bitcoin fell below $80,000. Analysts at BRN say the pattern resembles early 2022, when supply gradually shifted from weaker hands to long-term holders before a broader recovery cycle began.

Derivatives Market Points to Asymmetry

If volatility returns, derivatives markets suggest it could be amplified.

A 10% upward move in Bitcoin would liquidate roughly $4.3 billion in short positions, compared with about $2.4 billion in long liquidations on a similar downside move. In other words, short positions are currently more crowded, raising the possibility of a sharp short squeeze if sentiment turns positive.

Options pricing also reflects lingering uncertainty. March implied volatility, which traded near 40 before the latest selloff, climbed above 55 during the steepest drawdown and now sits around 48. While off its peak, volatility remains elevated compared with pre-selloff levels.

Macro Signals Offer Mixed Relief

The broader economic backdrop has provided some encouragement but not enough to shift the market’s mood.

Recent U.S. consumer price index data showed annual inflation cooling to 2.4%, slightly below expectations. Core inflation came in at 2.5%, matching forecasts. At the same time, January payroll data surprised to the upside, with 130,000 jobs added, nearly double projections.

That combination of easing inflation and resilient employment has left investors recalibrating expectations ahead of upcoming Federal Reserve minutes, GDP figures, and PCE data.

For now, liquidity remains tight and risk appetite subdued.

Bitcoin is down about 2% over the past week and more than 21% year-to-date, putting it on track for its weakest first quarter since 2015, based on partial data from CoinGlass. Ether is trading near $1,950, still below the $2,000 level after two consecutive weeks of heavy outflows.

As Misir put it, the market appears fatigued rather than panicked. With crowded short positions, fragile sentiment, and macro data still in flux, the next decisive move could be swift and significant. For investors, the current calm may be less a sign of stability and more a pause before renewed volatility.