Bitcoin is inching its way into the U.S. housing market, with mortgage giants Fannie Mae and Freddie Mac reportedly preparing to recognize it as an asset in mortgage applications. It’s a groundbreaking move that marks one of the clearest signs yet that crypto is being integrated into traditional finance. But there's a major caveat: only Bitcoin held on regulated U.S. custodial platforms will qualify.

This decision is part of a broader discussion underway at the Federal Housing Finance Agency (FHFA), which is exploring how crypto could be used as collateral in mortgage underwriting. For now, the agency is considering Bitcoin held on U.S.-regulated exchanges as proof of an applicant’s financial health—without requiring conversion to U.S. dollars.

A Step Forward—With Conditions

On the surface, the inclusion of Bitcoin in mortgage considerations appears to be a win for crypto adoption. But according to industry voices, the policy only acknowledges Bitcoin when it’s held in state-visible custody—leaving out a large share of long-term holders who practice self-custody.

Bitcoin held in cold wallets, multisig setups, or hardware devices won’t count toward a borrower’s financial profile. The system is only recognizing assets that are already embedded within the existing regulatory perimeter.

“This isn’t about adoption vs. resistance. It’s about adoption with conditions,” said Bitcoin financial services firm Swan. “You can play—but only if your Bitcoin plays by their rules.”

Self-Custody vs. Institutional Approval

Critics argue that excluding self-custodied Bitcoin undermines core crypto principles such as individual control, privacy, and sovereignty. Ownership of self-custodied Bitcoin is easy to verify cryptographically, but the mortgage system, for now, is opting for familiarity over flexibility.

“Self-custody is fundamentally aligned with American values,” wrote Nick Neuman, a specialist in sovereign crypto storage. “It’s trivial to prove ownership. Ignoring it is a mistake.”

Swan and other Bitcoin-native firms see this development as “phase two” of how legacy systems interact with disruptive technologies. In their view, traditional institutions initially resist innovation, later accept it under tight conditions, and eventually try to penalize those who don’t comply.

What This Means for Borrowers

The move signals a cautious embrace of digital assets in mortgage lending, but not a full shift. For now, only Bitcoin held on exchanges like Coinbase or other regulated platforms will enhance an applicant’s financial profile. This recognition could help some crypto holders qualify for a mortgage, especially those with sizable holdings on centralized platforms.

It’s important to note that the Bitcoin in question doesn’t function as loan collateral—it’s not something the lender can seize if a borrower defaults. Instead, it’s used to assess overall net worth and repayment ability, particularly in cases where income may fluctuate or employment is interrupted.

Looking Ahead

For Bitcoiners who value decentralization, the challenge is clear: either shift some holdings into compliant custody for short-term access to TradFi services—or hold firm to self-sovereignty and wait for the system to catch up.

Swan remains optimistic. As Bitcoin becomes more widely adopted, the firm believes that pressure will mount for lenders to recognize all forms of legitimate ownership, including cold storage.

“Eventually, the most secure form of money will unlock the most flexible capital,” Swan noted. But until then, the mortgage market will continue to favor visibility over autonomy.

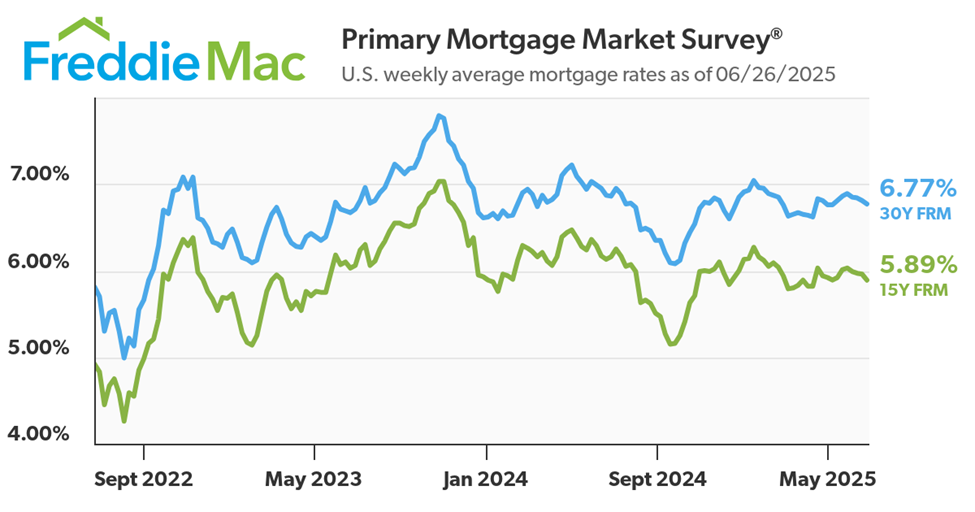

Chart of the Day