Algorithmic trading has changed the way crypto traders execute large orders. Instead of placing everything at once and moving the market, algorithms can split trades into smaller chunks, reducing slippage and making execution smoother. On Binance, two of the most widely used algo strategies are Time Weighted Average Price (TWAP) and Percentage of Volume (POV).

To see how these tools perform in the real world, Binance analyzed roughly 25,000 anonymized trades across different assets, sizes, and configurations. The results offer valuable insights for traders considering whether algo orders might give them an edge.

What Are TWAP and POV?

- TWAP (Time Weighted Average Price):

Executes a trade evenly over a set period of time. For example, a one-hour TWAP spreads an order across that hour to reduce sudden price swings. - POV (Percentage of Volume):

Executes based on market activity. If set at 10%, the algorithm will try to match 10% of the market’s trading volume during the chosen period. This makes it more adaptive than TWAP, especially in fast-moving markets.

Both are designed to minimize slippage—the gap between the expected price and the actual execution price.

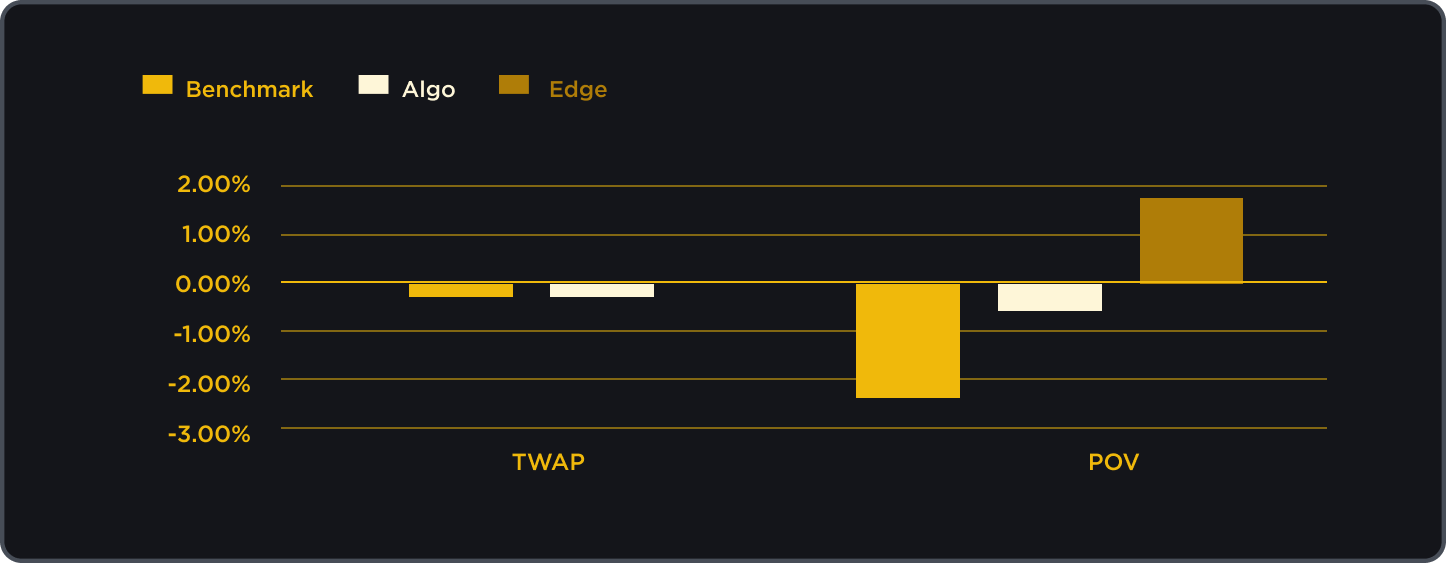

Case Study 1: Overall Performance

Across all assets and trade sizes, the data showed:

- TWAP: Very similar results to simple market orders, with an average edge of -0.01%.

- POV: A clear advantage, reducing slippage by 1.81% compared to benchmarks.

The takeaway? POV generally outperformed TWAP in aggregate, but performance varied based on asset type and trade size.

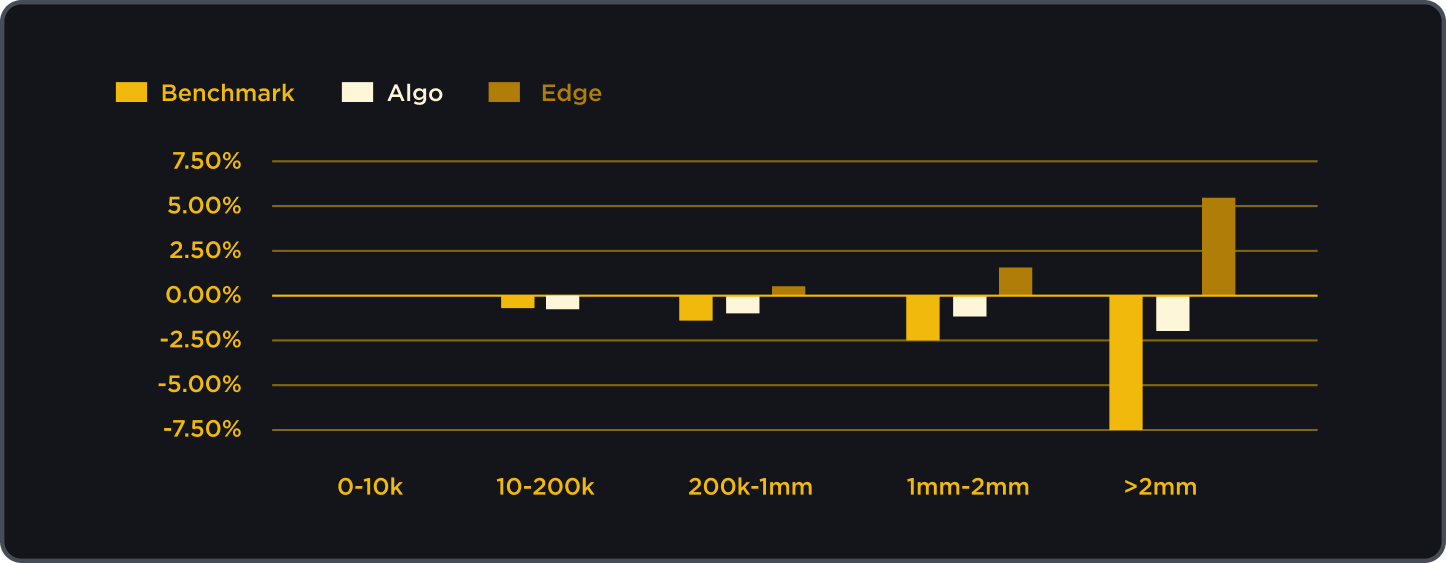

Case Study 2: The Role of Trade Size

Bigger trades naturally suffer higher slippage. For orders above $2 million, slippage in market orders reached as high as -7.4%. Algo orders proved most useful in these cases:

- On illiquid assets, POV achieved average improvements of up to 13%.

- On liquid assets like BTC and ETH, small trades didn’t benefit much—and in some cases, algo settings actually hurt performance.

This suggests algo trading shines where liquidity is thin and trades are large.

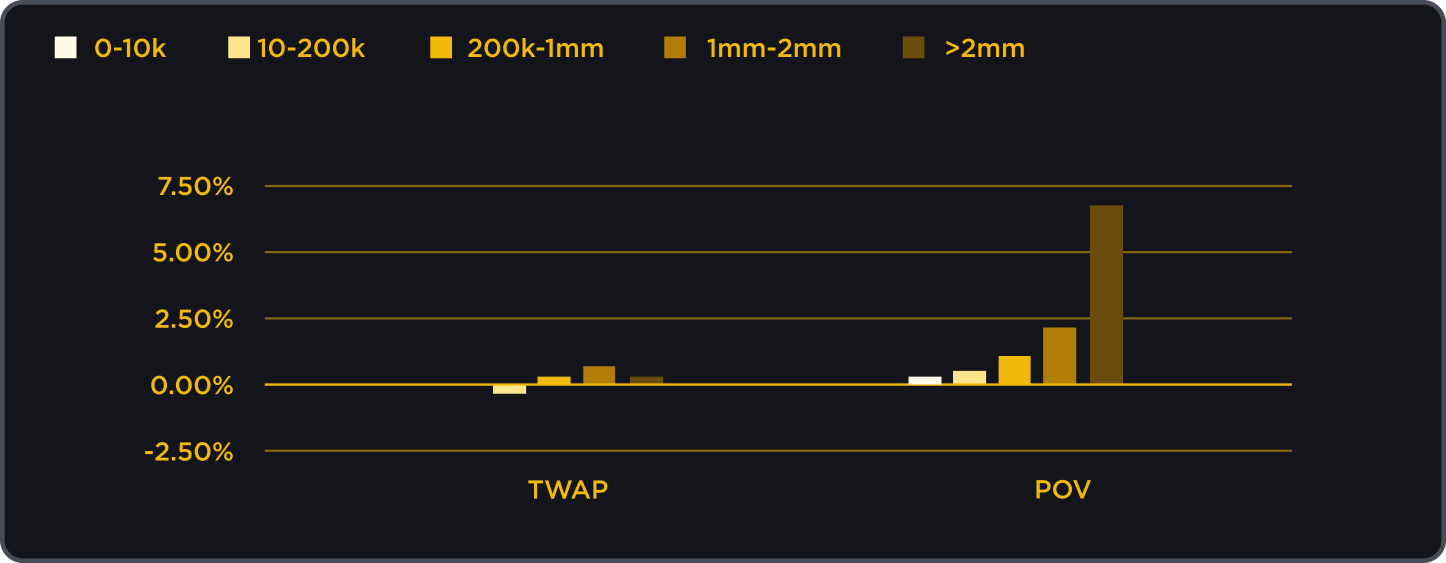

Case Study 3: TWAP vs. POV

- POV adapts to market activity, often outperforming TWAP on large orders.

- TWAP, while simple and predictable, can lag if set with overly long durations, especially on liquid markets where orders could be filled quickly.

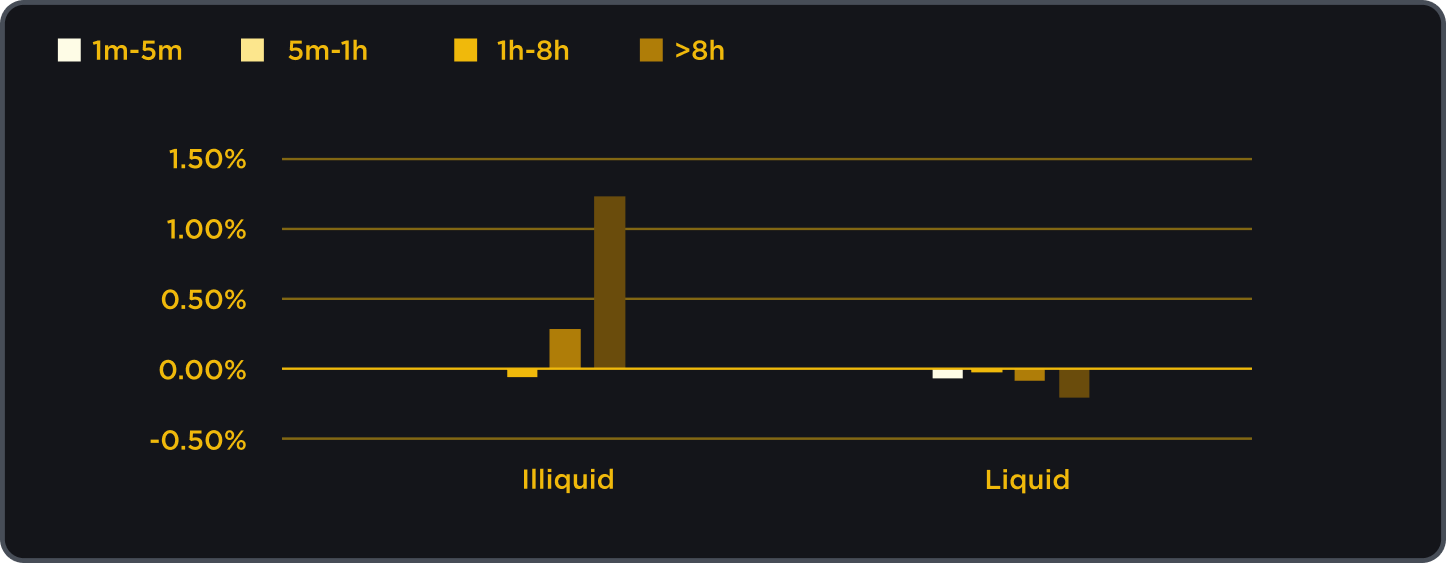

One trade-off: POV trades can take longer to finish, sometimes up to 8 hours, making speed a factor for strategy selection.

Case Study 4: The Importance of Configuration

A key finding was that configuration matters as much as the strategy itself:

- TWAP duration: Setting a duration that’s too long in liquid markets increased slippage unnecessarily.

- Limit price settings: Algo orders with a limit price performed significantly better, as they paused execution during sharp price swings and resumed once conditions stabilized.

These adjustments helped traders avoid hidden costs and market volatility.

Key Takeaways

- Large, illiquid trades benefit most from algo orders, especially POV.

- Small, liquid trades may be better off with simple market orders.

- Careful configuration—such as setting an appropriate duration and using limit prices—can make a meaningful difference.

- Beyond slippage reduction, algo orders can also disguise large trades by breaking them into smaller pieces, reducing market visibility.

Closing Thoughts

Binance’s TWAP and POV strategies highlight both the potential and the pitfalls of algorithmic trading. Used wisely, they can help traders control slippage, reduce costs, and manage execution risk. But they aren’t plug-and-play solutions—success depends on choosing the right tool for the trade and configuring it carefully.

For professionals handling size or trading less liquid tokens, these strategies may be essential. For smaller trades in deep markets, the old-fashioned market order often works just fine.